Overview

Join the thousands of property professionals who rely on RP Data to master the property market, grow their business and provide superior insights to clients.

Property data trusted by government, banks and real-estate professionals

Access over 40 years of curated property data on Australia’s largest independent property and analytics data platform. View recent sales and listings, access models to interpret the data, and enhance your business strategy with deep market insights.

Property data trusted by government, banks and real-estate professionals

Access over 40 years of curated property data on Australia’s largest independent property and analytics data platform. View recent sales and listings, access models to interpret the data, and enhance your business strategy with deep market insights.

With an extensive range of property attributes, RP Data delivers powerful real estate insights. Search granular listings data, download detailed property and suburb reports, compare suburb profiles and discover market trends.

Built on the CoreLogic data universe, we ingest over 7,000 data sources into the RP Data platform. With coverage across over 10m properties, 600k+ sales & 550k+ rental transactions per year and over 1 million new data points each month.

Master your local market like never before with new data insights and suburb statistics, resulting in more informed conversations and decisions.

Search using specific or broad terms – by number of bedrooms, right up to complete state and region searches, and receive the results in seconds.

Benefit from substantial checks and processes that ensure our data’s quality.

Produce valuations and confident market appraisals efficiently

With a wide view of the property market you can continually learn, grow and improve your business or investment strategy. Find new ways to stand out from the competition, identify potential growth suburbs or provide valuable insights to your clients to continually build your relationships.

Produce valuations and confident market appraisals efficiently

With a wide view of the property market you can continually learn, grow and improve your business or investment strategy. Find new ways to stand out from the competition, identify potential growth suburbs or provide valuable insights to your clients to continually build your relationships.

Download detailed digital property and suburb reports with more images, comparable properties and tracking than static pdfs. Compare suburb profiles and discover market trends.

Digital reports also give you information on what has been viewed and when, leading to more informed and timely conversations if you are sending reports to customers.

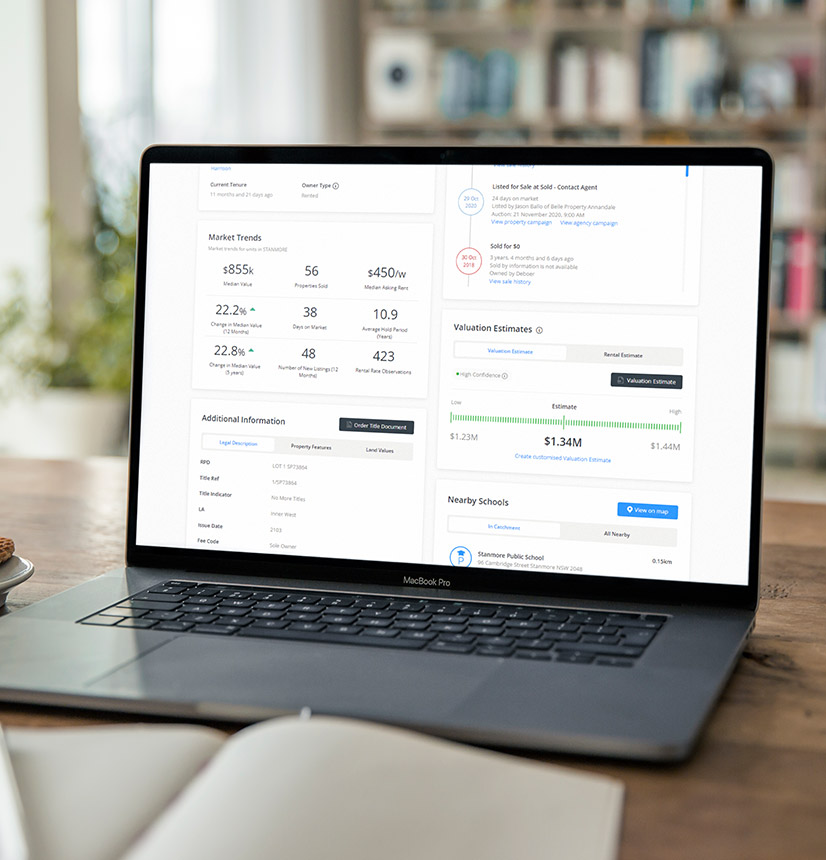

Determine the value of properties or portfolios with AVM reports featuring a value-estimate range, confidence score, past sales of similar nearby properties, and suburb statistics.

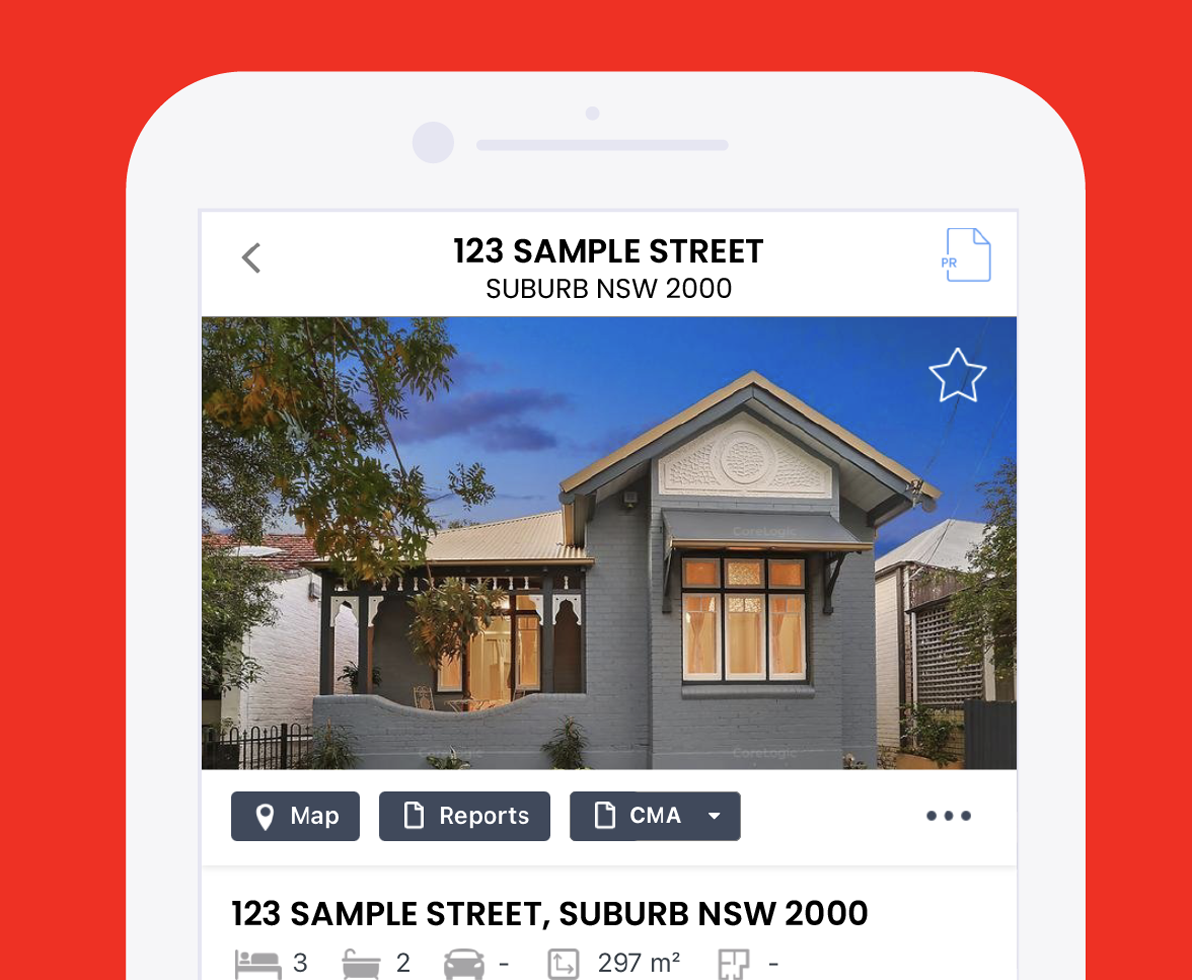

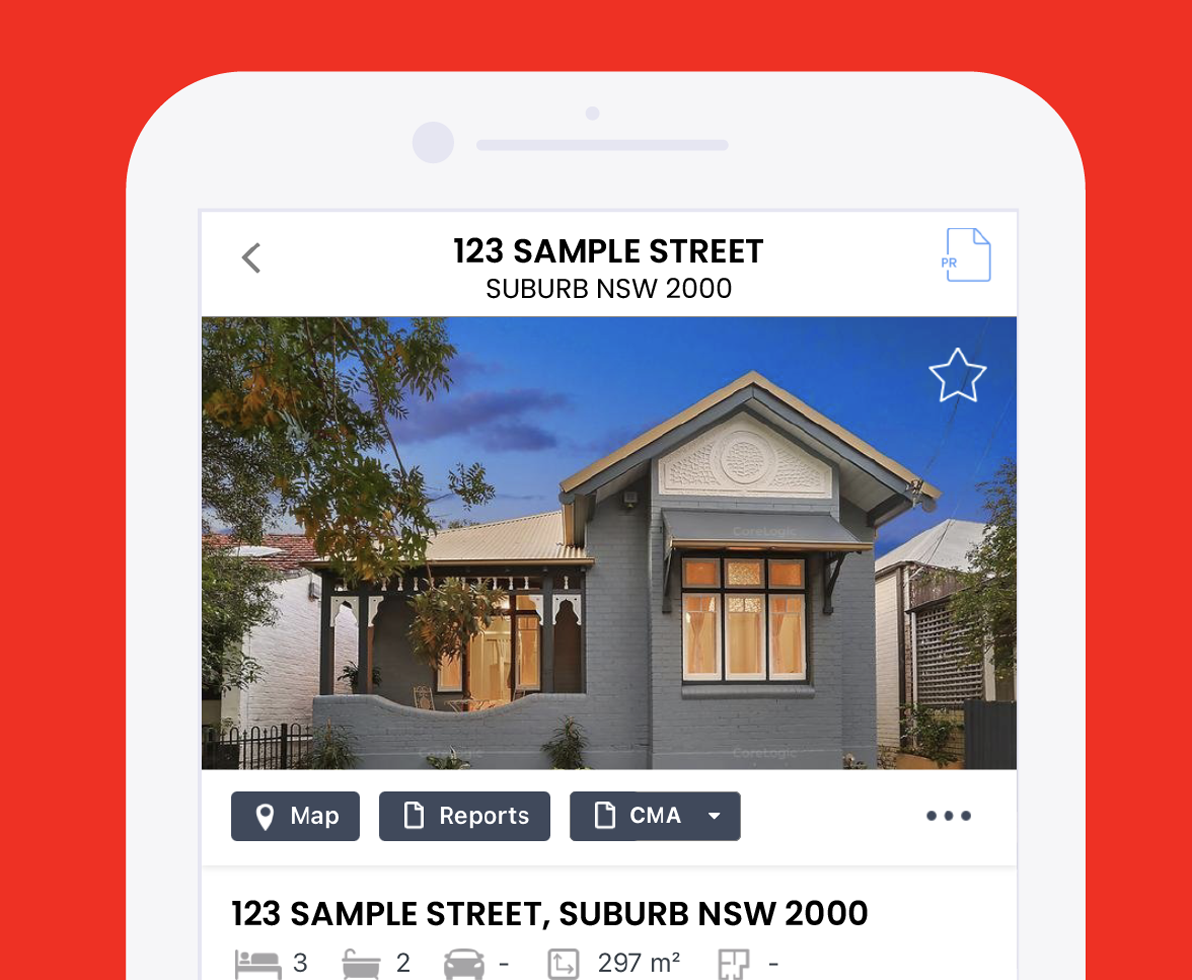

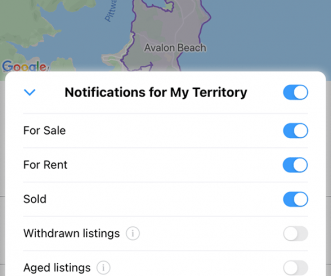

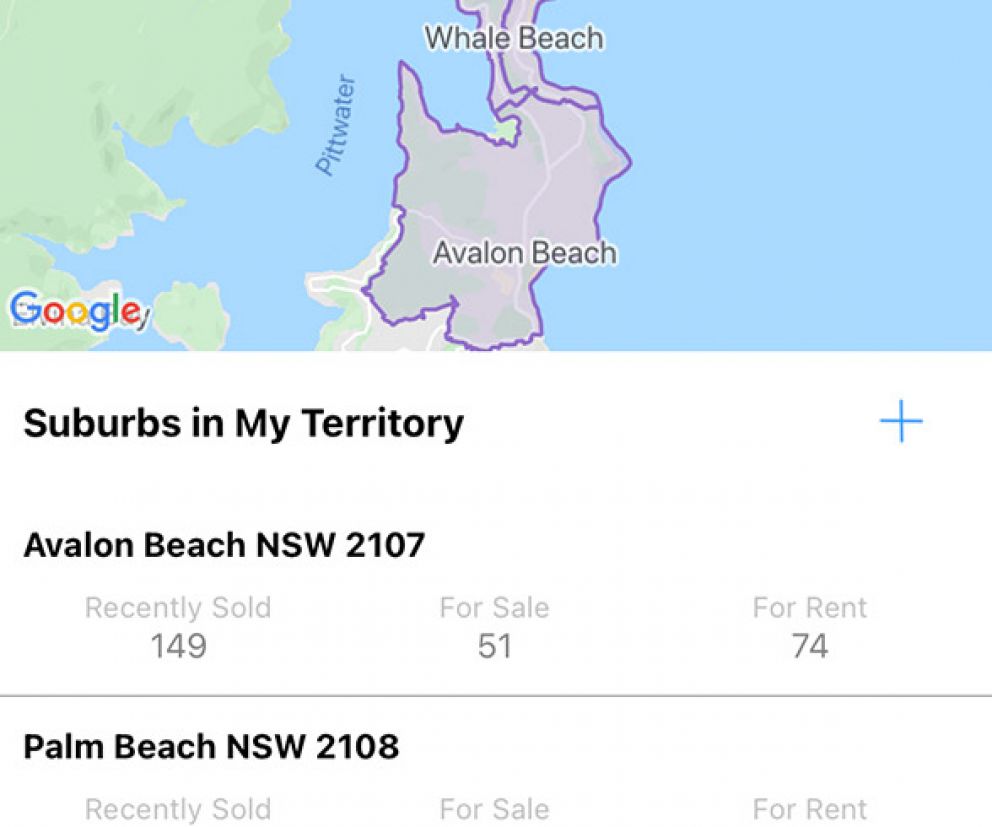

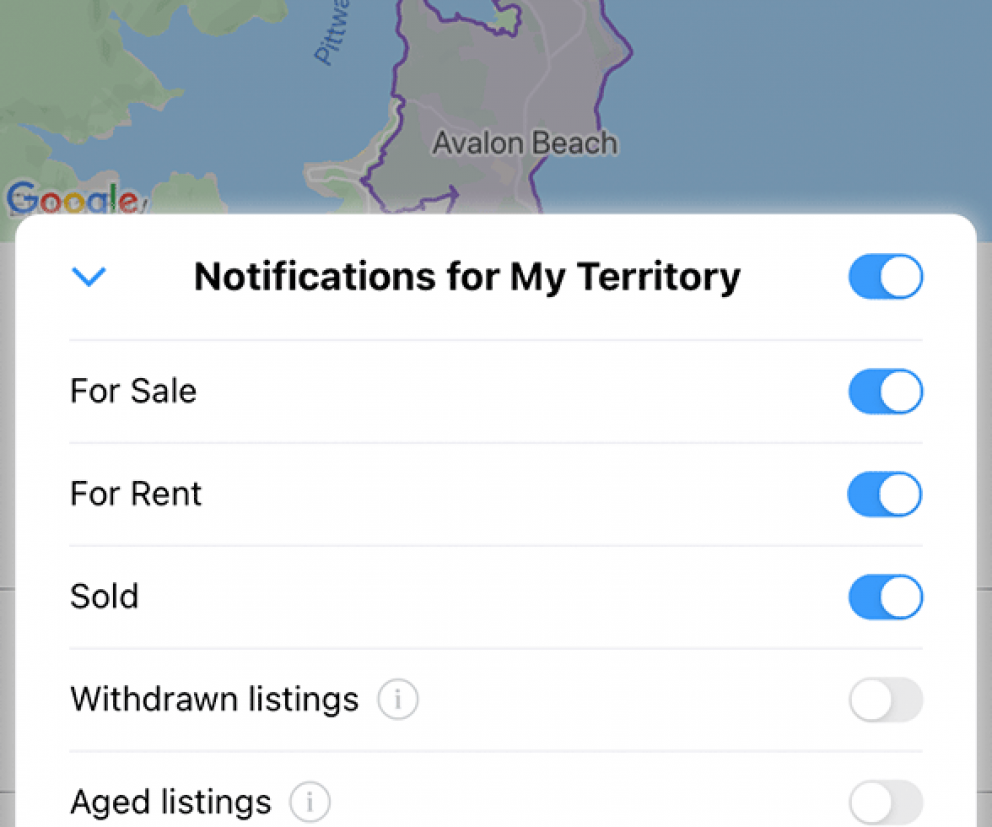

Have the power of the desktop application to hand anywhere, anytime with the RP Data Mobile app. Access property details, suburb trends, customisable searching, and the ability to produce CMAs and reports all while on the go.#

Access insights on the go

With the RP Data Mobile App, you can enjoy ‘on the go’ access to property details and values, deep market insights and customisable searching and reporting. Available with any RP Data package.

View Pricing

Model the data and achieve high-value insights

Perform advanced analysis directly within RP Data, with models to interpret the data, unlocking insights that help you identify market trends.

Model the data and achieve high-value insights

Perform advanced analysis directly within RP Data, with models to interpret the data, unlocking insights that help you identify market trends.

Master your local market like never before with new data insights and suburb statistics, resulting in more informed conversations with your clients and increased customer satisfaction.

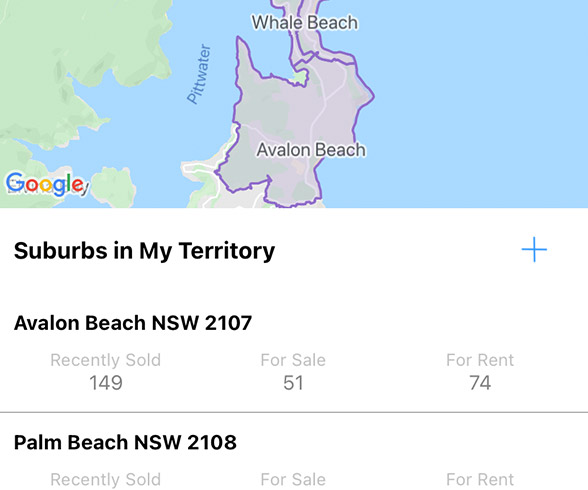

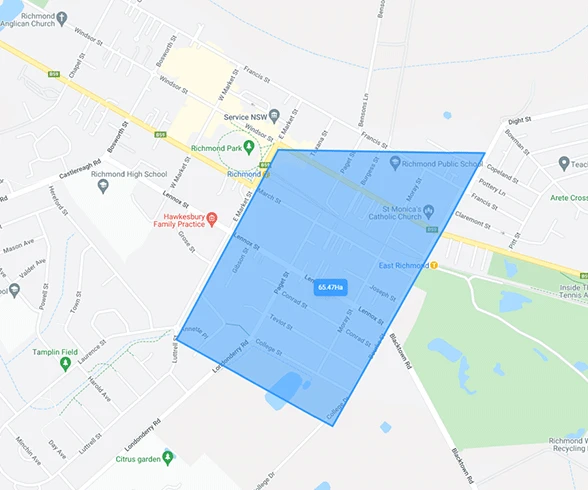

Simply plot your area onto a map and receive insights, data and generate reports specific to your area of interest.

With innovative mapping technology, find distances to schools and amenities, measure property boundaries, identify property features, show aerial and cadastral maps, and access development applications.

Track specific properties or areas with Watch Lists and be notified of any market changes or new listings.

Automate processes and improve your focus

Automate daily processes and focus on more important tasks. RP Data lets you track your prospects and makes it easier to manage and report on listings, recent sales and current rentals.

Automate processes and improve your focus

Automate daily processes and focus on more important tasks. RP Data lets you track your prospects and makes it easier to manage and report on listings, recent sales and current rentals.

Automate monitoring of selected properties and be alerted of any changes to automated value estimates.

Combine our powerful data with your CRM databases for a superior customer view, to help you to target the right clients.

With the ability to export data in CSV format, you can further filter and analyse the data offline.

Packed with features

Check out how you can power your real estate business with these features

Advise your client on the estimated value of their property or portfolio

Featuring a value estimate range, confidence score, past sales of similar nearby properties and a suburb statistics snapshot, our AVMs contain the information you need to help you expertly advise your clients on the estimated value of their property or portfolio.

Showcase your high level of service and validate your selling and purchasing price recommendations with trusted and verifiable data.

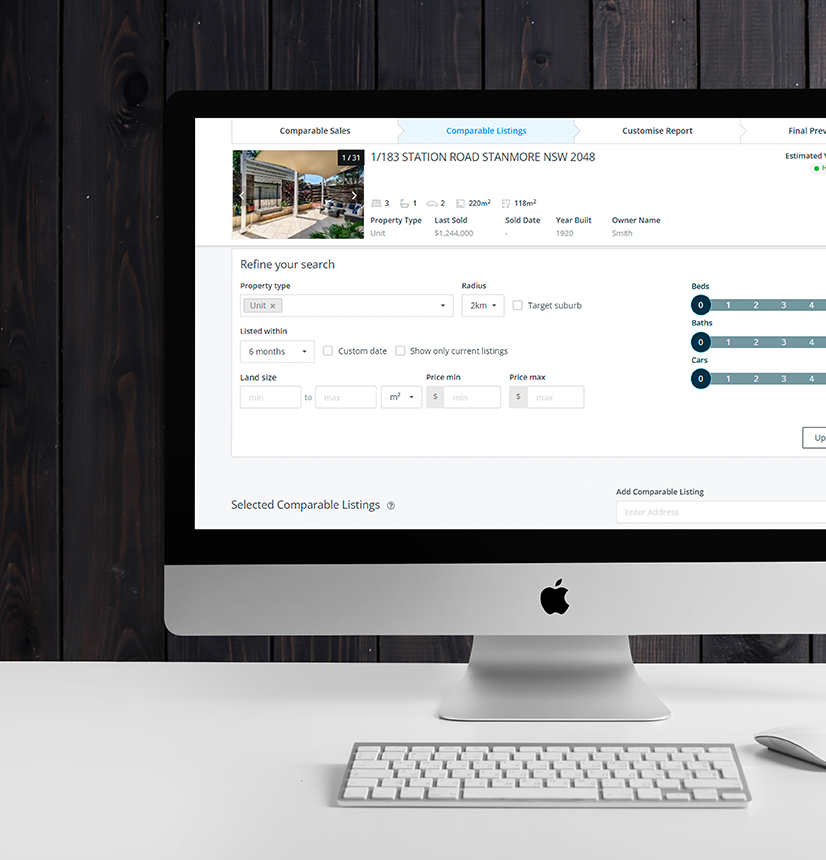

Make confident property market price estimates

The Comparative Market Analysis report, or CMA, helps thousands of agents and brokers every month demonstrate their market knowledge and expertise in a customised, professional report for clients and prospects.

Have confidence in the estimated market price you provide to your clients for their property sale or lease, with data-based evidence and current factors that are likely to affect the pricing. Easily find comparable sales, recent rental listings and on-market properties with full property history from RP Data.

Marketing contacts for more effective marketing strategies

Personalise your direct marketing activity and target potential listings more effectively. Marketing Contacts gives you access to data collected in compliance with privacy laws, such as personalised address details that could dramatically increase the response rates from your direct mail campaigns.

In addition, you can access phone numbers to call people who haven’t signed up to the Do Not Call register. Distinguish between those who are likely to list or not, based on certain attributes, or those who are likely to be tenants or owner occupiers.

Property data in your pocket

Enjoy ‘on the go’ access to property details and values, deep market insights and customisable searching and reporting with the RP Data Mobile App. Research the market while grabbing a coffee with a client, create and deliver reports between meetings, and respond to enquiries immediately from any location.#

Packed with features

Check out how you can power your real estate business with these features

Advise your client on the estimated value of their property or portfolio

Featuring a value estimate range, confidence score, past sales of similar nearby properties and a suburb statistics snapshot, our AVMs contain the information you need to help you expertly advise your clients on the estimated value of their property or portfolio.

Showcase your high level of service and validate your selling and purchasing price recommendations with trusted and verifiable data.

Make confident property market price estimates

The Comparative Market Analysis report, or CMA, helps thousands of agents and brokers every month demonstrate their market knowledge and expertise in a customised, professional report for clients and prospects.

Have confidence in the estimated market price you provide to your clients for their property sale or lease, with data-based evidence and current factors that are likely to affect the pricing. Easily find comparable sales, recent rental listings and on-market properties with full property history from RP Data.

Marketing contacts for more effective marketing strategies

Personalise your direct marketing activity and target potential listings more effectively. Marketing Contacts gives you access to data collected in compliance with privacy laws, such as personalised address details that could dramatically increase the response rates from your direct mail campaigns.

In addition, you can access phone numbers to call people who haven’t signed up to the Do Not Call register. Distinguish between those who are likely to list or not, based on certain attributes, or those who are likely to be tenants or owner occupiers.

Property data in your pocket

Enjoy ‘on the go’ access to property details and values, deep market insights and customisable searching and reporting with the RP Data Mobile App. Research the market while grabbing a coffee with a client, create and deliver reports between meetings, and respond to enquiries immediately from any location.#

Latest news and research

More News & Research

Auction Market Preview - 28 April 2024

Auction volumes steady for fourth consecutive week

Improvement in preliminary clearance rate across combine… Improvement in preliminary clearance rate across combined capital cities

Preliminary clearance rate slips across similar auction … Preliminary clearance rate slips across similar auction volumes week-on-week

Solid bounce back in preliminary clearance rate Solid bounce back in preliminary clearance rate

Packages & Pricing

1 The CoreLogic Service provided for Business trials is only available for business customers who hold a valid ABN. Business trial requests are subject to CoreLogic's approval. The Trial Period and geographic access provided as the CoreLogic Services for your Business trial will vary at the discretion of your CoreLogic Salesperson, and your access will automatically be disconnected at the end of your Trial Period.

2 Eligible CRMs or PropTech Solutions currently include:

3 Capped at 10,000 properties/month

Terms and Conditions

Lite Package available for 1,3 and 5 users. Base Premium and Pro packages available for 1, 3, 5, 10, 15 and 25 users.

Note: Some features are currently available in RP Data Professional only, and will be transitioned to RP Data in due course. CoreLogic intends that users will continue to have access to these features (if included in the user’s chosen package) during and after this transition.

Note: Agency Benchmark Reports (ABR). Available in subscriptions for Agencies only. Please note that the sales, listings and agent information used to calculate the analytics in the ABR report may not be recorded or available for all residential properties at the time of publication, and supply of ABR is subject to the CoreLogic Disclaimers. CoreLogic cannot guarantee that the Customer's specific agency information will appear in the ABR.

How can we help you?

Let's get this conversation started! Our team is here to provide you with more information and answer any questions you may have.

Request a callback

Terms & Conditions

#Supporting mobile operating systems: iPhone - Requires iOS 12.0 or later. iPad - Requires iPadOS 12.0 or later. iPod touch - Requires iOS 12.0 or later. Mac- Requires a Mac with Apple M1 chip and macOS 11.0 or later. Android- Requires 7.0 and up.